ESG, climate, and sustainability reporting standard-setters are taking their time updating and communicating guidelines. While that can feel frustrating when you’re a company trying to keep up with best practices – it honestly might not be a bad thing.

A little more than a week ago, EFRAG, the European regulator at the helm of the CSRD, released its draft list of European Sustainability Reporting Standards (ESRS) datapoints. There are more than 1,100! That’s… a lot. About 260 are voluntary, but it’s still a lot.

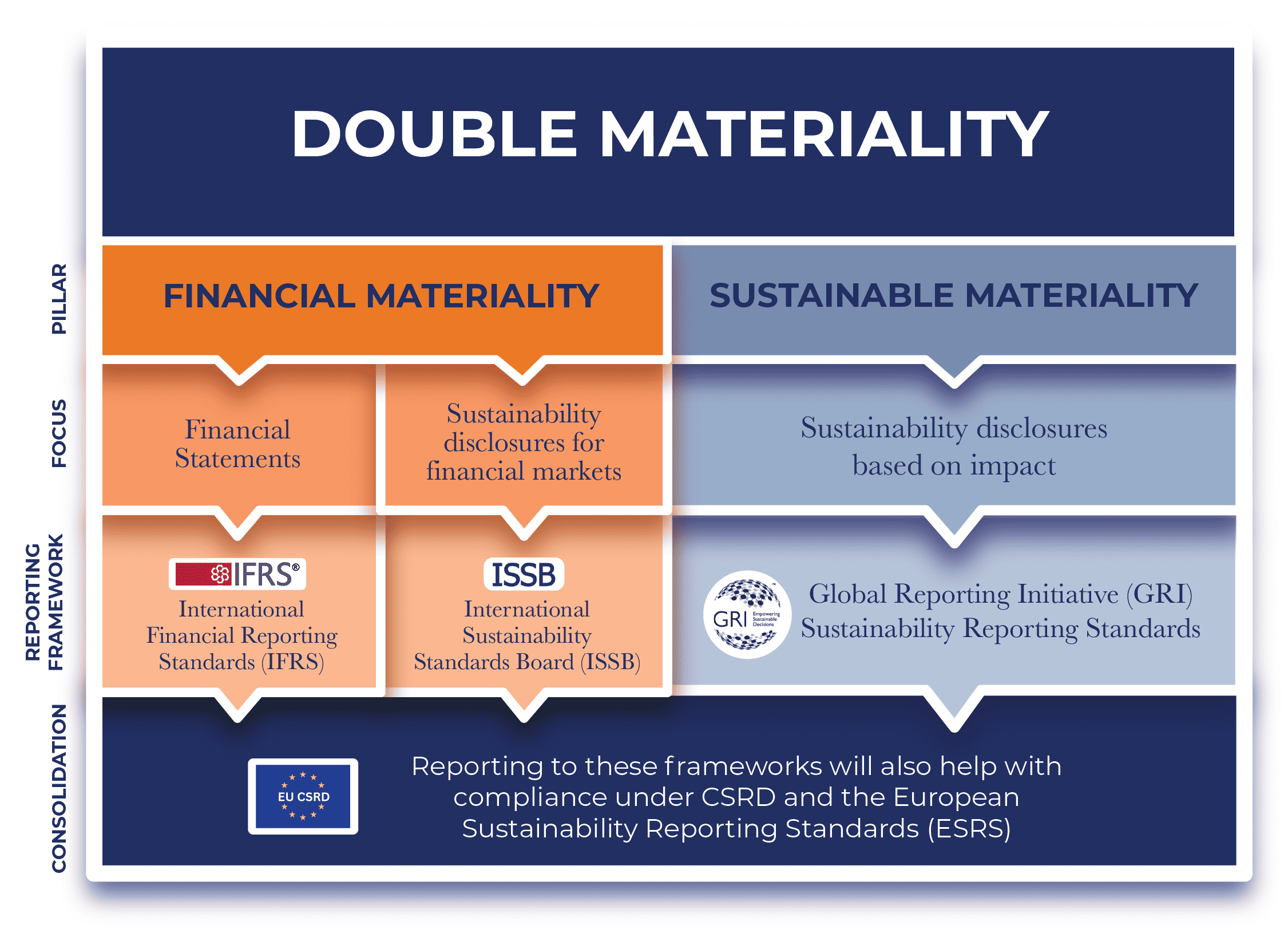

Embedded in these 1,178 datapoints is the concept of double materiality, which combines two often distinct camps under one proverbial roof.

One camp is concerned with information relating to a company’s impacts on the environment, people, and the economy. While the other focuses on how those externalities (environment, people/society, and the economy) affect the company. In a previous blog, we discussed the comprehensiveness of CSRD requirements and interoperability of the most prominent frameworks and their corresponding standards.

While the initial 12 ESRS are in draft form, legislation passed by the EU Parliament dictates companies meeting a certain criterion must disclose in accordance with the framework beginning in 2025, citing ’24 data. As tends to be the case in this arena, it appears some corporates were caught off guard.

Why the Delay with Sustainability Reporting Standards?

In advance of releasing the ESRS datapoints, EFRAG announced it was postponing additional ESRS reporting standards – sector-specific standards.

Some misunderstood this announcement to mean that CSRD requirements were being postponed, while others took this announcement as an opportunity to throw stones at the mandate’s validity. The latter posits that the initial set of standards is somehow flawed or incomplete. A majority welcomed the news as it will give companies in certain sectors more time to understand the general requirements and cross-cutting standards. However, parent companies operating outside the region have stayed mum but are most likely stressed as they remain in limbo about knowing what will be required in terms of time and resources.

Are Sustainability Standards Typically Delayed?

Yes, the incremental release and re-polishing of sustainability standards is common.

GRI, the de facto sustainability reporting framework, has undergone several evolutions over the years. The new IFRS/ISSB sustainability standards have only released S1 and S2. The SEC is still considering its final climate-related disclosure rule.

It’s important to remember that this is not unique to non-financial or ESG disclosures. This type of process has precedent across the business community. For instance, the Generally Accepted Account Principles (GAAP) have undergone similar evolutions and continue to implement amendments.

Patience is a Virtue

For a long, long time, the promise of consolidated sustainability standards and reporting frameworks was the holy grail. As recently as a year ago, sustainability practitioners saw the harmonization of standards as a real possibility.

Now, that may not be the case. Instead, EFRAG, the SEC, GRI, and IFRS each release iterations of their varied standards when they’re good and ready. And importantly, their standards ideally reflect best practices and the needs of various stakeholders.

Perhaps the ideal of homogenous reporting standards was always a fantasy. Corporates are required to report to different stakeholders in different ways, constantly. We should be prepared for the same when it comes to sustainability reporting and ESG disclosures. After all, we should be grateful that the discipline has matured to a place where there are a select number of reporting standards and frameworks and that they all start in the same place. They are built on the same foundation of issues and ideas. With the right people on the case, companies that can report to one requirement should be able to report to multiple with efficiency and ease.

Are you looking for specific recommendations for your company regarding ESG disclosures and sustainability reporting? Reach out to us today – we’re always happy to chat!